A chargeback is a charge returned to a payment card after a customer successfully

disputes an item on their account statement or transactions report. A chargeback may occur on

debit cards (and the underlying bank account) or on credit cards. Chargebacks can be granted to

a cardholder for a variety of reasons.

There was an error submitting the form. Please try again.

;

Excellent

based on 2115 reviews

Amelia

20 feb 2022

I recently worked with Hire Coworker, and their service was outstanding. The team was

professional, efficient, and always willing to do extra work to ensure my needs were

met. Highly recommend them and their Virtual Assistant.

Benjamin

5 Dec 2021

Hire Coworker helped me find the best developer for my project. Their virtual assistant

was professional and efficient. Actually, I was very satisfied with the outcome. They

have top-quality developers.

James

1 Jan 2022

I recently worked with Hire Coworker to find a financial expert for my business, and I am

extremely satisfied with my virtual assistant. The team was professional, knowledgeable,

and helped me find the best fit for my company. Excellent service and the best virtual

assistant provider...

Emma

15 March 2022

Hire an e-commerce store developer and Tony Capo both use these guys for virtual

assistant and I can honestly say we are pleased with the results. No complaints; highly

recommended; and confidently recommended. Friendly Behavior and great customer service.

Henry

2 June 2022

I found Neil at Hire Coworker to be extremely knowledgeable, professional, and thorough

in his follow-up. No matter what time is on watch..

Their virtual assistant service is extremely valuable. Neil is so intelligent, reliable,

and on time.

I have renewed my contracts more than once to use Hire Coworker's services in the

future.

Lucas

28 Oct 2022

Hire Coworker has been great at helping me design and launch my websites and graphic

design projects. Hire Coworker's virtual assistant has saved me money, energy and lots

of time. My business is running smoothly and he is now my friend. Everyone needs a

virtual assistant from Hire Coworker.

Noah

15 feb 2023

have been using Hire Coworker for 1 year now, and I love it. when I've ever called in

for their virtual assistant. It has been taken care of immediately. Their virtual

assistant always takes care of the problem.

Olivia

2 feb 2023

Hire Coworker team is amazing and they offer fantastic service at a very good price. My

virtual assistant name is Saif, completes tasks to a high standard and always has great

ideas and suggestions for online marketing and social media. I highly recommend Hire

Coworker to any business owner who wants to start delegating tasks to help move their

business forward.

DIGITAL MARKETING PROCESS

A Simple, Iterative Process

RESEARCH

We do Keyword research as per the niche of the website. We also do the analysis of competitor

websites.

CREATING PLATFORM

1. After analysis, we placed the keywords in our website content and website URL'S.

2. We create a strategy, which keywords we focused on more.

3. How we can generate leads.

How we work

i. We do only white hat SEO ii. We generate high traffic on website (organic & paid

traffic)

iii. For keywords ranking improvement, we work on high DA, TA, PA websites.

iv. Increase the ranking of keywords & increase traffic on websites.

Tools we use

We use Google webmaster (To check the website health)

Google analytics (To track the website traffic)

Google AdWords (for google ads and Keywords planner

tools for keywords research)

HIRE COWORKER

The Numbers Do the Talking

3500+

Successful Project

750+

Certified PHP Developers

8+

Year's Industry Experience

600+

Satisfied Global Clients

HIRE SEO SPECIALISTS ONLINE WITH EASY STEP

Talk To Us

What sort of graphic design position are you seeking?

Handpick Best Expert

We provide screened CVs of the Graphic Designing experts we've chosen.

Build Your Team

Phone or video conference interviews of selected candidates are available. You may assign

tests to them.

Get Going

If you are pleased with the results, immediately hire them and get to work.

How do we understand chargebacks?

Chargebacks are done for charges that have been fully processed and settled. They

must be

reversed through an electronic process involving multiple entities. As a result, they can take several

days to

settle and return to the original account fully.

The chargeback process is similar across most credit card networks and issuing

banks, with

specific differences for each bank or network. A chargeback works from the issuing bank through the card

network and

to the merchant's acquiring bank. The merchant can decide to dispute the chargeback or accept it.

Chargebacks are a consumer protection tool that allows consumers to get their

moneyback for

fraudulent charges or purchases that don’t live up to standards by submitting a dispute with their card

issuer.

If you notice a transaction on your credit card account that doesn’t look familiar

or run

into

issues with a recent order, you may want to (and should) dispute the transaction. Generally, you’ll have

two

options

when disputing a transaction: refund or chargeback.

A refund comes directly from a merchant, while a chargeback comes from your card

issuer.

When to ask for a chargeback

A chargeback is the payment amount returned to a debit or credit card after a customer disputes

the

transaction.

The merchant or the cardholder’s issuing bank can initiate the chargeback process.

Merchants typically incur a fee from the card issuer when a chargeback occurs.

Federal law requires card issuers to offer chargebacks within 60 days of the billing date.

In cases other than fraud, you may be able to resolve your issue directly with the merchant

rather

than by requesting a chargeback from your bank.

Charges can be disputed for many reasons, such as

A cardholder being charged by a merchant for items they never received

A merchant duplicating an order by mistake

Mistaken costs caused by a technical issue

Fraudulent charges from credit or debit card information that has been compromised

What Is the Chargeback Process?

The primary participants in the chargeback process are the cardholder, the merchant,

the

issuing bank, the acquiring bank, and sometimes the credit card network.

The cardholder/customer

These may be the same individual, but only sometimes. The cardholder is the actual

owner

of the payment card used to purchase the dispute. The customer is the individual who placed the

transaction.

In a typical transaction or a friendly fraud chargeback, the cardholder and the

customer

are the same person. In an actual fraud scenario, the customer who made a transaction with a stolen card

is

not the same person as the cardholder who disputes it later.

1) The merchant

is the individual or company who sold a product or service to the customer. When the

chargeback is filed, the merchant must decide whether to accept or dispute it.

2)The issuing bank (Issuer):

A bank or other financial institution that issues a branded payment card to the

cardholder. Examples: Bank of America, Wells Fargo, Capital One.

3)The acquiring bank (Acquirer)

The merchant’s bank holds their merchant account and enables them to accept credit

card

payments.

4)The credit card network:

The association that owns the credit card brand used in the transaction. The four

major

credit card networks in the United States are Visa, Mastercard, American Express, and Discover. These

networks set the terms for credit card transactions, followed by the issuing banks.

Other companies that service merchant accounts, such as payment processors and

gateways,

may also become involved in the chargeback process.

What is Chargeback Processing?

The merchant or the cardholder’s issuing bank can initiate the chargeback process.

If started with a merchant, the process is similar to a standard transaction; however, the funds are

taken from a merchant’s account and deposited with the cardholder’s issuing bank.

How Do You Fight a Chargeback?

When a customer initiates a chargeback, the merchant has a set period to respond.

This varies by the payment processor but is usually around 30 days. At this time, the merchant can

provide the signed receipts, contracts, and any other documentation that shows that the chargeback is in

error.

Why do chargebacks happen?

When a credit card company issues a chargeback, they use a code to indicate the

reason for the reversal. There are four general chargeback code categories:

Fraud

Quality

Clerical

Technical

1) Fraud

Chargebacks exist to make it safer for customers to shop. They protect against other

fraudulent purchases made without the buyer’s knowledge or consent. Fraud is the most common reason for

a chargeback.

Chargebacks with the following reason codes have been requested due to fraudulent

activity:

Chargeback reason

American Express reason code

Discover reason code

Visa reason code

Mastercard reason code

The card wasn't present at the time of the transaction

F29

UA01

10.4

4834

Counterfeit Europay, Mastercard, or Visa (EMV) card

F30

UA05 or UA06

10.5

4870

The card was not present at the time of the transaction

F29

UA06

10.4

4863

EMV card was lost, stolen, or not received at the time of the transaction

F31

None

None

4871

2) Quality

Chargebacks also keep retailers accountable. If a buyer receives a defective product

or never receives the item they paid for, they can initiate a chargeback.

In many cases, no proof of delivery or an illegal returns policy will mean a

customer is entitled to a chargeback.

An increasing number of merchants are offering product or service subscriptions.

While free trials are great for encouraging customer sign-ups, you can be hit with chargebacks if

subscriptions aren’t cancelled promptly when requested.

Chargeback reason

American Express reason code

Discover reason code

Mastercard reason code

Visa reason code

Defective goods and services

C32

RM

None

13.3

Goods or services were not as described

C31

RM

None

13.3

Goods or services were not as described

C08

RG

4855

13.1

3) Clerical:

A clerical chargeback can be raised if a buyer is billed twice for an item or a

return is made without a refund.

Chargeback reason

American Express reason code

Discover reason code

Mastercard reason code

Visa reason code

Invalid card number

P01

IN

4834

12.1

Incorrect transaction amount

P05

AW

4846

12.4

Duplicate charges

P08

DP

4999

12.6

4) Technical:

If there’s an issue with the buyer’s bank or credit card, or they don’t have funds

in their account, a technical chargeback may be issued.

Website errors and confusing checkout processes can also cause technical

chargebacks. To combat this problem, use a reliable e-commerce solution with a hassle-free checkout.

Limits distractions at the checkout so customers know exactly what they’re buying.

Chargeback reason

American Express reason code

Discover reason code

Mastercard reason code

Visa reason code

Invalid card number

F10

UA01

4837

10.1

Missing signature

F14

UA02

4840

10.2

What is friendly fraud?

Illegitimate chargebacks (friendly fraud)

Sometimes, customers will initiate chargebacks despite receiving their purchases.

Termed “friendly fraud,” illegitimate chargebacks can occur because consumers are

unhappy with their products, are confused about payments, or are simply trying to gain a free product.

It’s estimated that 61% of all chargebacks happen due to friendly fraud.

Nicolas Tranchant, founder of jewellery store Vivalatina, says, “The biggest reason

for our chargebacks has been the client’s dishonesty. Sixty per cent of them are claimed without even an

email to explain a problem with the jewellery we had shipped to them, with no explanation and no intent

to allow us to solve the issue.”

In these cases, merchants can dispute customer chargebacks to regain funds.

How do you dispute a chargeback?:

Respond as quickly as possible when disputing a chargeback since delayed action may

result in a chargeback loss.

1) Gather information

Identify the customer and transaction in question when you’re notified of a

chargeback. Source as much information about the transaction as possible, including warehouse data and

delivery status.

You can also contact the customer directly to see if their issue can be resolved.

2) Submit your chargeback response

If you feel that a chargeback has been made unfairly, you can submit your evidence

in a dispute response.

This document is returned to the bank or card issuer that sent you the chargeback

letter (alternatively, you may need to initiate your own chargeback dispute). Follow any formatting

instructions and deadlines, and ensure you directly respond to the chargeback’s

reason code.

For disputed fraud or “no authorisation” chargebacks, provide evidence that the

cardholder was aware of and authorised the transaction. AVS (address verification system) matches, CVV

confirmations, signed receipts, or contracts may help to prove this.

3) Await the decision

After you submit a rebuttal, the situation is out of your hands while the

processor’s acquiring bank reviews the information. The cardholder’s bank makes the final decision about

whether it will process the chargeback, and it will inform the customer of its decision.

4) Disputing chargebacks

Consumers benefit from the protection chargebacks provide against fraud and poor

customer service.

Chargeback rules promote fair return policies and discourage retailers from selling

subpar products. But, when consumers abuse the chargeback system, merchants can face unexpected losses

and fees.

Merchants can recover disputed funds by submitting evidence to a consumer’s credit

card company, showing that the customer authorised the transaction and received their purchase.

What is Chargeback handling?

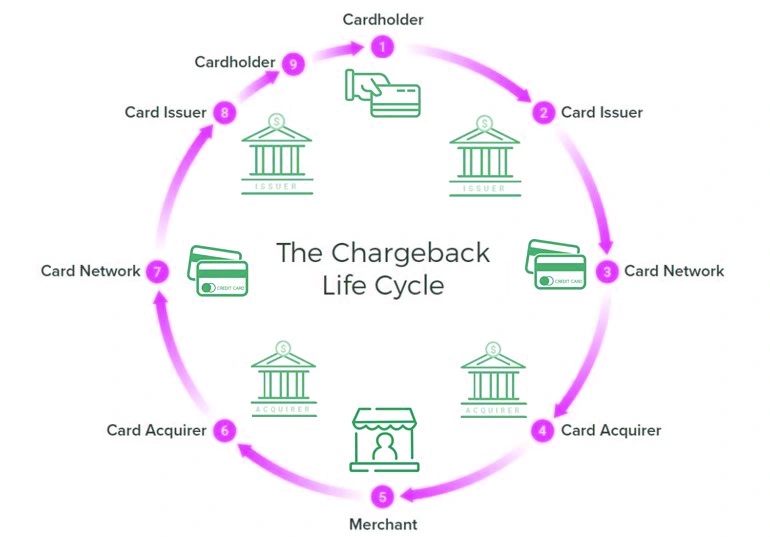

1) What is Process flow?

As depicted in the below process flow, a chargeback will complete a full circle. It

is initiated by the cardholder and issuing bank, and ultimately, your response will be presented to the

cardholder and issuing bank.

English

Legible

The professional look and feel

Structured and organised format

How do ACCOUNTING CHARGEBACKS work?

The initial chargeback—the reversal of the transaction the cardholder is

disputing—should be posted to Accounts Receivable. This positions each chargeback as funds owed to

you and which you expect to recover. You can also create a special designation for this, such as

“Accounts Receivable Chargebacks.”

What is CHARGEBACKS INSURANCE?

A chargeback occurs when an agent has to pay back a portion of their commission

because their client passes away or cancels an insurance policy early. Each company's chargeback

schedule and contract is slightly different, and chargeback rules vary by product line.

EXPERTS

HIRE OUR

BEST DIGITAL MARKETING EXPERT

Edward C.

Digital Marketer

4.3/5

A accomplished IT specialist with more than 7 years

experience in the banking, fintech, enterprise, etc.

Linkedin

B2B

Marketing Strategy

Lead Generation

Technical SEO

6+

Syed K.

Digital Marketer

4.7/5

SEO Executive with 10+ years of experience working on

projects that were mission-critical.

Google Data Studio

Web Analytics

Google Ads

eCommerce

SEO Writing

10+

Kristine S.

Digital Marketer

4.5/5

Social Media Manager at the senior level with nearly 6

years of diverse digital marketing expertise.

With the help of SEO and PPC, Hirecoworker's was able to boost online leads by more than +260% and boost overall traffic to the new website by +364%.

Aaron. G

These men are amazing. They have assisted us in expanding our firm, and now the biggest issue we are experiencing is having too much business, which is the ideal situation.

Marcio. M

Hirecoworker is a much-needed blessing that has far surpassed our expectations. They are trustworthy, up front, and quick to attend to all of your demands. You can rely on them, and most importantly, they deliver on their promises with no holds barred

Robert. S

Hirecoworker is a much-needed blessing that has far surpassed our expectations. They are trustworthy, up front, and quick to attend to all of your demands. You can rely on them, and most importantly, they deliver on their promises with no holds barred.

FAQs

Do You Have Questions

What is an SEO expert?

An SEO expert or SEO specialister finds methods, tactics, and procedures to

boost the number of website visits and seeks to get a high-ranking placement in search

engine results such as Google or Bing. Creating more leads for the organization opens up new

avenues for profit and growth.

Why would you hire a virtual SEO assistant?

If you lack the ability to develop keyword-rich SEO material, you will not

maximize your Google ranks. Use a virtual assistant to avoid monthly retainer fees and the

necessity to engage an onsite person, which will cost you extra. Let your virtual assistant

to handle your Search Engine Optimization by examining critical data like as page visits,

bounce rates, backlinks, link building activities, and other SEO chores such as writing blog

articles and other related material. You may utilize the internet and other platforms to

reach your target consumers, giving you the opportunity to expand your company faster.

What are the advantages of hiring an SEO Virtual Assistant?

Expert search engine optimization may significantly boost your ranks. Spend less

money since hiring a virtual assistant is more cost-effective over time. You may devote more

time to your main tasks.

What is the difference between SEO and SEM?

SEO (search engine optimization) is sometimes used as a catch-all word for SEM

(Search engine marketing). SEM, on the other hand, refers to sponsored advertising. As a

result, the two words should be distinguished. This is because SEM is about delivering

bought traffic to a website, but SEO is about bringing organic traffic to a site and

monitoring traffic trends.

What factors contribute to effective SEO?

The primary driver of search engine results is high-quality, authoritative

content, and there is no alternative for unique and excellent material. This is especially

true while performing SEO marketing. Excellent content for your target audience increases

site traffic, increasing the relevance and authority of your site.

Lot's of experts is ready to work remotely, Hire Coworker help people to get VA in least price. Virtual Assistants are an affordable alternative to hiring specialized employees to perform tasks, handle operations or provide services for the company...

Virtual Assistants report higher job satisfaction rates and a better work-life balance. The virtual employee model creates a low-stress, high-productivity work environment.